The Redistribution Curve

A mirror of the Laffer curve for AI-era economies that shows there is a level of redistribution that maximises profit.

AI creates a situation where capital owns both labour and the means of production (agents build agents, robots build robots). What follows shows that there is a demand-side mirror image of the Laffer curve where it’s not just a case of too much tax reducing public sector revenue, but too little redistribution reducing private sector profits.

A few disclaimers: yes there are more radiologists with AI, but there aren’t many elevator operators these days. Technology creates and destroys jobs but has always created more. The pie grows. But this time might be a bit different, the jobs might not be there unless the pie is grown through redistribution.

This is not the traditional zero-sum idea of sharing a slice of a finite pie rather than seeing the economy grow, it is specifically a way to share the rewards AND maximise profits.

Everyone wins. This is a way to have your pie and eat it.

Laffer and a level of taxation for maximum state revenue

The informal version of the Laffer curve says that if income is taxed at zero percent, the state collects nothing. If income is taxed at one hundred percent, the state may also collect nothing, because people have little reason to earn taxable income when every pound they earn is taken. Two zero endpoints force a peak between them: revenue rises with the rate, then falls.

The formal version rests on a single behavioural number. Write revenue as the rate times the base, R = t·B, and let the base shrink as the rate climbs, because people work, invest, and report less, or leave, when taxed harder. If the base has constant elasticity e, the revenue-maximising rate is:

The existence of the Laffer curve is not in dispute. Where its peak sits is, because no one agrees on the value of e, and the whole politics of supply-side economics lives inside that one contested parameter.

What follows builds the same kind of object from the demand side, with the same kind of single contested number, and arrives at the opposite policy conclusion: that in a fully automated AI-era economy there is a level of redistribution that maximises profit. If Laffer says there is a maximum workable tax, this says there is a minimum workable redistribution, and successful economies must operate in the Goldilocks zone between the two.

A level of redistribution for maximum private-sector profit

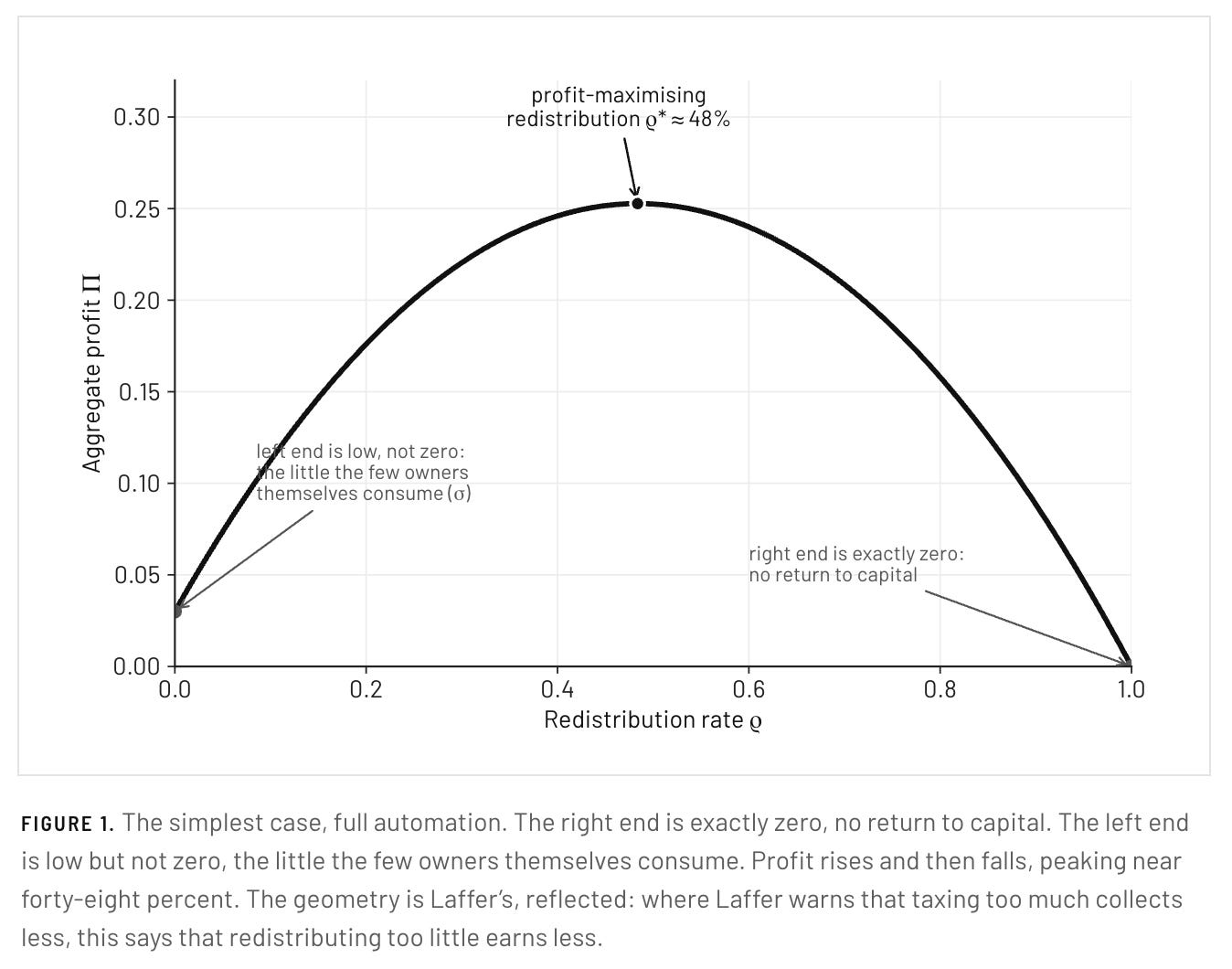

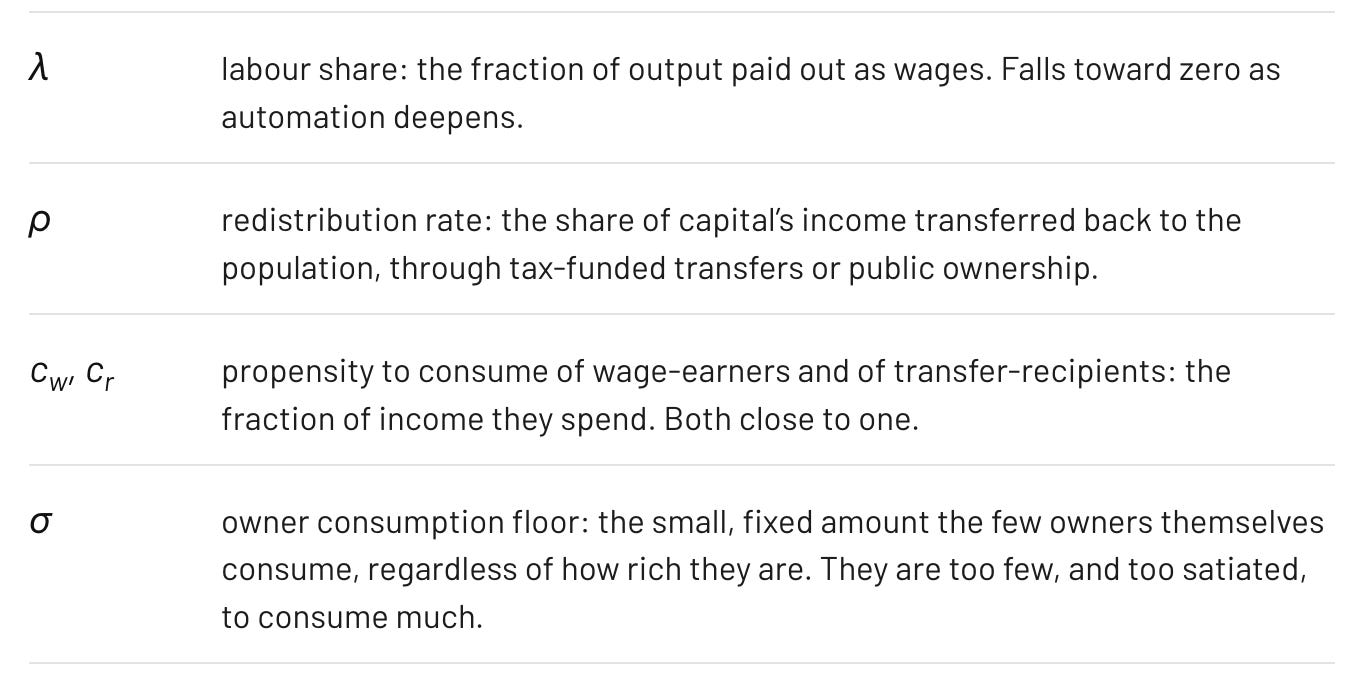

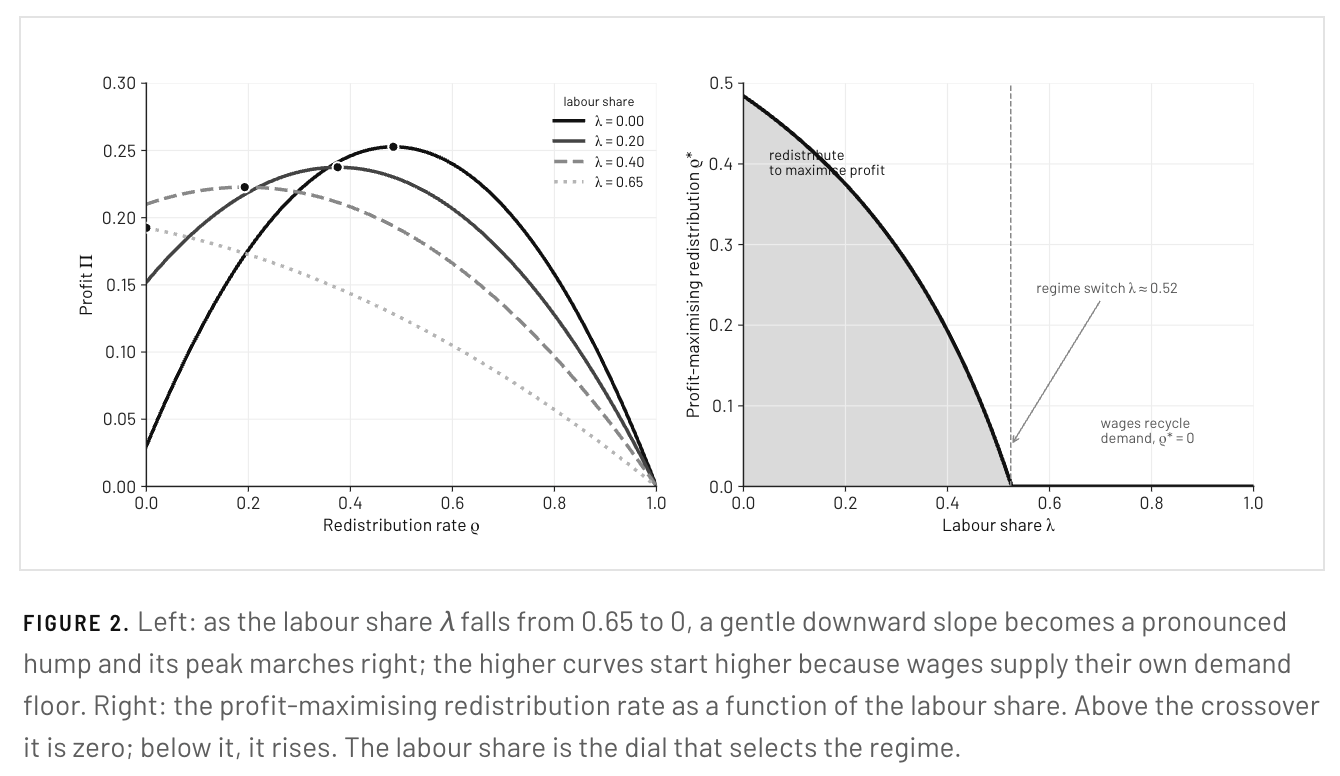

Take the limiting case first: full automation, where capital owns labour outright. Software agents write the software, robots build the robots, models train the models. Labour’s share of income falls to zero. Now ask what aggregate profit does at the two extremes of redistribution, where the redistribution rate ρ is the share of capital income taxed or otherwise transferred back to the broad population as universal income, public dividends, and the like.

Unlike the Laffer curve, the two ends are not quite symmetric, and the asymmetry matters. At ρ = 1 the return to capital is zero by definition, so profit is exactly zero. At ρ = 0 profit is not zero but low: with no wages and no transfers, the only buyers are those who hold the capital, the owners, and a small number of satiated owners can absorb only a little of what is produced in an economy where production costs fall without labour and mass production for everyone, not just the elite, becomes possible. Realised profit falls to a floor set by the collective owners’ own consumption. Call that floor σ, a small quantity. One end pinned at zero, the other end low, and the curve rises and then falls between them. That is enough to make a hump, and its peak is the maximum profit.

In a demand-constrained economy realised sales equal what people choose to spend. Let recipients of redistribution consume a fraction cr of what they receive, close to one because they spend nearly all of it. Then demand is the owners’ floor plus what recipients spend, owners keep the untaxed share, and profit is:

This is the structural mirror of Laffer’s t* = 1 ÷ (1 + e). The peak sits a little below one half, pulled down from exactly one half by the owners’ own consumption σ. The smaller the owners’ consumption, the closer the peak is to fifty percent.

How the model is built

The mechanism is a single accounting loop with one premise behind it. The premise is that the economy is demand-constrained: the machines can make more than enough, so what limits realised output is not capacity but whether anyone has the income and willingness to buy. When demand falls short of capacity, the amount actually produced and sold equals the amount demanded. Normalise potential output to one, so every quantity below is a share of what the economy could produce.

Income arrives in three streams and is spent according to who holds it. Wages are λ, and wage-earners spend cwλ. Capital’s share of output is the remainder, 1 − λ; of that, a fraction ρ is redistributed and the rest, 1 − ρ, is retained by owners. Recipients spend cr of what they receive, which is ρ(1 − λ). Owners add their fixed floor σ. Total demand is the sum:

Because the economy is demand-constrained, realised output equals C. Of the value of that output, capital’s claim is its share 1 − λ, of which owners keep the part not redistributed, 1 − ρ. So realised profit is capital’s kept share of whatever actually gets sold:

The tension is that ρ appears twice, with opposite signs. Raising it lifts demand C, because transfers put income into hands that spend it, so more output is sold. Raising it also shrinks the fraction owners keep, 1 − ρ. More redistribution means a larger pie that is sold but a smaller slice retained. The profit-maximising rate is the point where those two effects balance, found by setting the derivative to zero. At full automation, λ = 0, this reduces to the curve in the previous section.

The result is a mirror image of the familiar defence of free markets, that they raise inequality but lift absolute incomes for the poorest. This reduces inequality but still maximises gains for the richest.

The labour share switches between the two regimes

Full automation is the limit, and the present has not reached it. With the labour share λ in the model, wages provide a demand floor of their own, because wages are spent. Carrying λ through the optimisation gives a profit-maximising rate that depends on it:

When the labour share is high, wages do the recycling, the optimal redistribution is zero, and ordinary supply-side logic holds. As the labour share falls, the peak moves, and below a crossover the profit-maximising redistribution climbs toward one half. Automation does not break the Laffer logic. It shifts the economy along a family of curves, from the regime where low taxes serve capital best into the regime where sufficient redistribution does.

AI automates cognition, not only muscle

The labour share held roughly constant for a century, and its stability was sometimes read as an unwritten law, when in reality it was a property of the kind of automation on offer. The waves of innovation of the industrial era substituted for human muscle while still needing human cognition to direct it. The Industrial Revolution mechanised manual work, but a person operated the loom, drove the locomotive, ran the machine. Cognition stayed a complementary human input, and because the machine made that input more productive instead of unnecessary, wages rose alongside output. Capital and labour climbed together. That complementarity, not an iron law, is why labour’s share held.

The information era repeated the pattern. Post-industrial economies, even those associated with manufacturing such as Germany, became primarily services-based. Radio, television, computers and the internet created jobs because the services that could be provided expanded, and inside that expanding pie there were humans in the loop and new roles to fill: a bigger pie of automation with enough jobs inside it.

Artificial intelligence is a phase change, with the possibility of removing the second input altogether and fully automating cognition as well as manual work: it directs the machines, writes the software, makes the decisions human operators used to make. Once the complementary factor is itself automated, there is no remaining task at which mechanisation makes a human more valuable. That is what potentially lets the labour share go where it never has, toward zero, and it is why the demand-side regime, a curiosity while only muscle could be automated, takes over.

The model does not cover every job. Nurses and pop stars sell human presence, which stays scarce and commands a premium, though only in finite supply. The claim is about the jobs where the pie of production expands: where profits must flow to the masses to create new demand, and where production needs few humans in the loop.

The early signs are visible. Returns to capital are pulling ahead of labour as technology-sector network effects switch from distribution, where users beget users, to production, where software writes software. Capital flows upstream onto larger and larger balance sheets and infrastructure providers, while firms lay off programmers. The risk is not yet realised, and full automation may never complete, but it is the scenario to prepare for.

What the labour share is, and where it has gone

The labour share is the part of national income that reaches people because they work, wages and salaries, as opposed to the part that reaches people because they owned something the production used, profit, interest, and rent. It is the workers’ slice of every dollar the economy produces, measured at the moment income is earned in production.

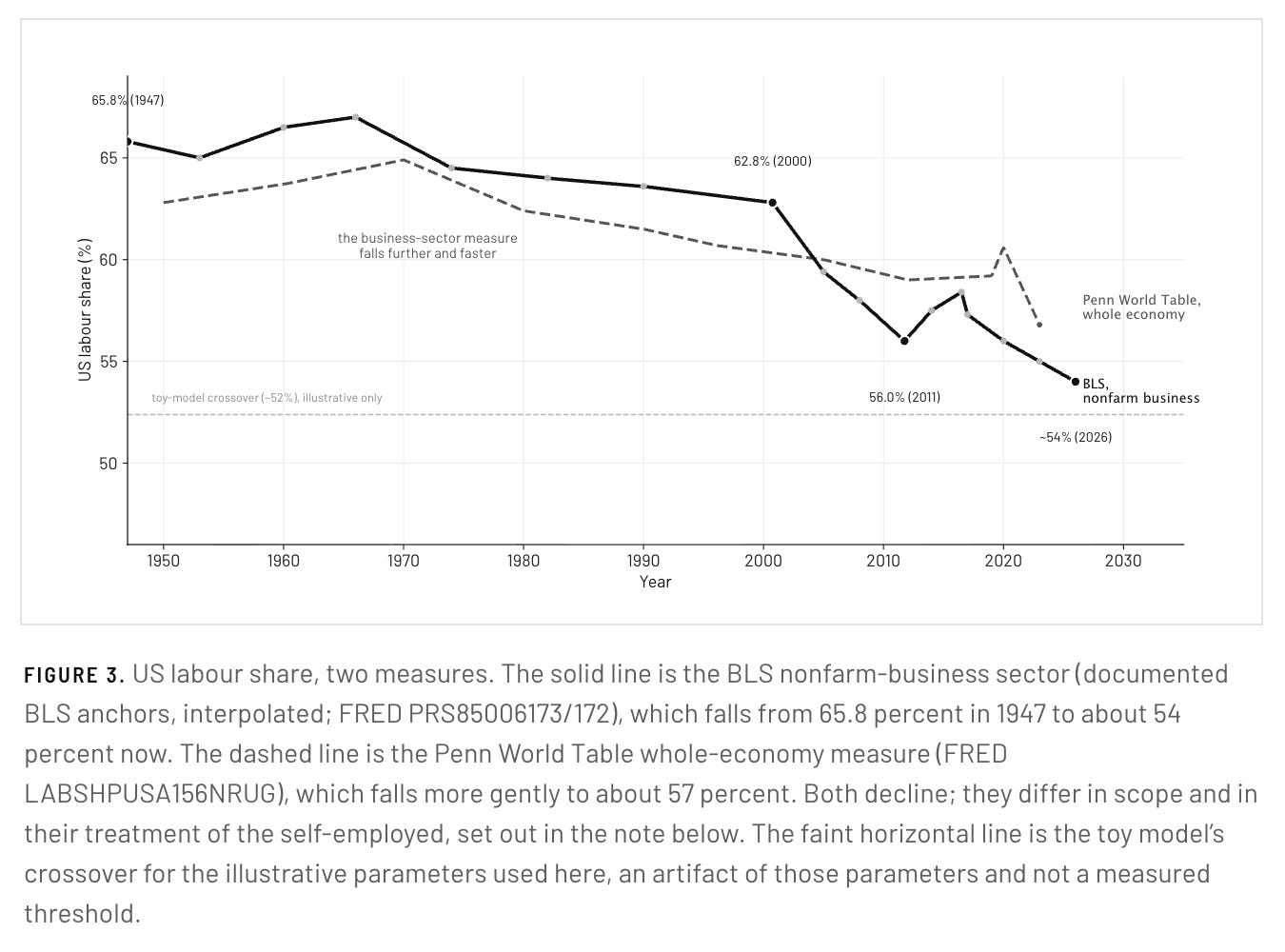

For the United States nonfarm business sector it was 65.8 percent in 1947 and held near that level for half a century, one of the steadier numbers in macroeconomics. It was still 62.8 percent at the end of 2000. Then it broke. It fell below 60 percent by 2005, reached a low of 56.0 percent in 2011, recovered partway to 58.4 percent by 2016, and on the most recent readings sits back near 54 percent, the bottom of the postwar range.

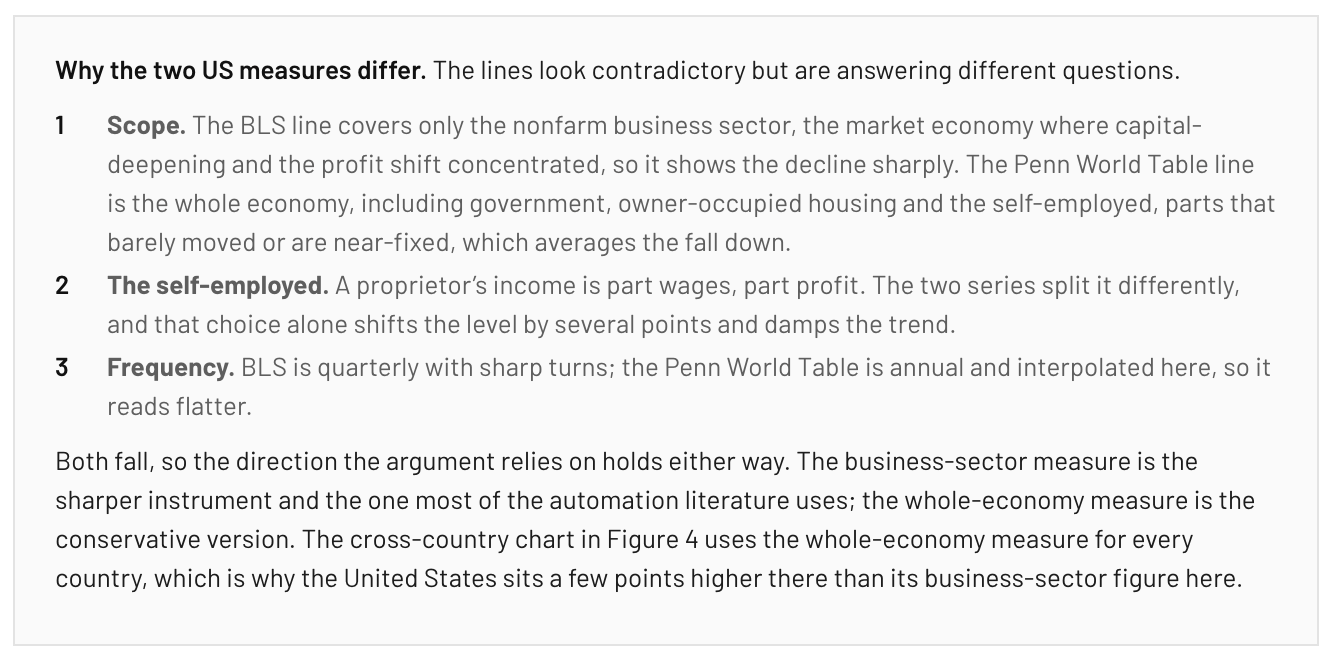

That is the business-sector measure. On the broader whole-economy measure the fall is gentler, from about 63 percent to 57 percent, but the direction is the same. The two measures, and the reasons they differ, are shown together in Figure 3 and the note beneath it.

These charts do not say the economy has already reached the demand-side peak. They say the effects of AI are about to kick in. If the trend accelerates past the point the curve says exists, a point set by the labour share, the economy crosses a threshold where redistribution raises profit, replaces the lost labour income, and everyone wins. The model’s crossover from tax limits to redistribution minimums is a function of made-up propensities and should not be read as a precise line the data has or has not crossed. The measured fact is the direction and speed of travel before AI: the share has fallen for twenty-five years under ordinary automation and globalisation. The thesis is that AI steepens the decline, because it can substitute for cognition entirely.

The same direction everywhere

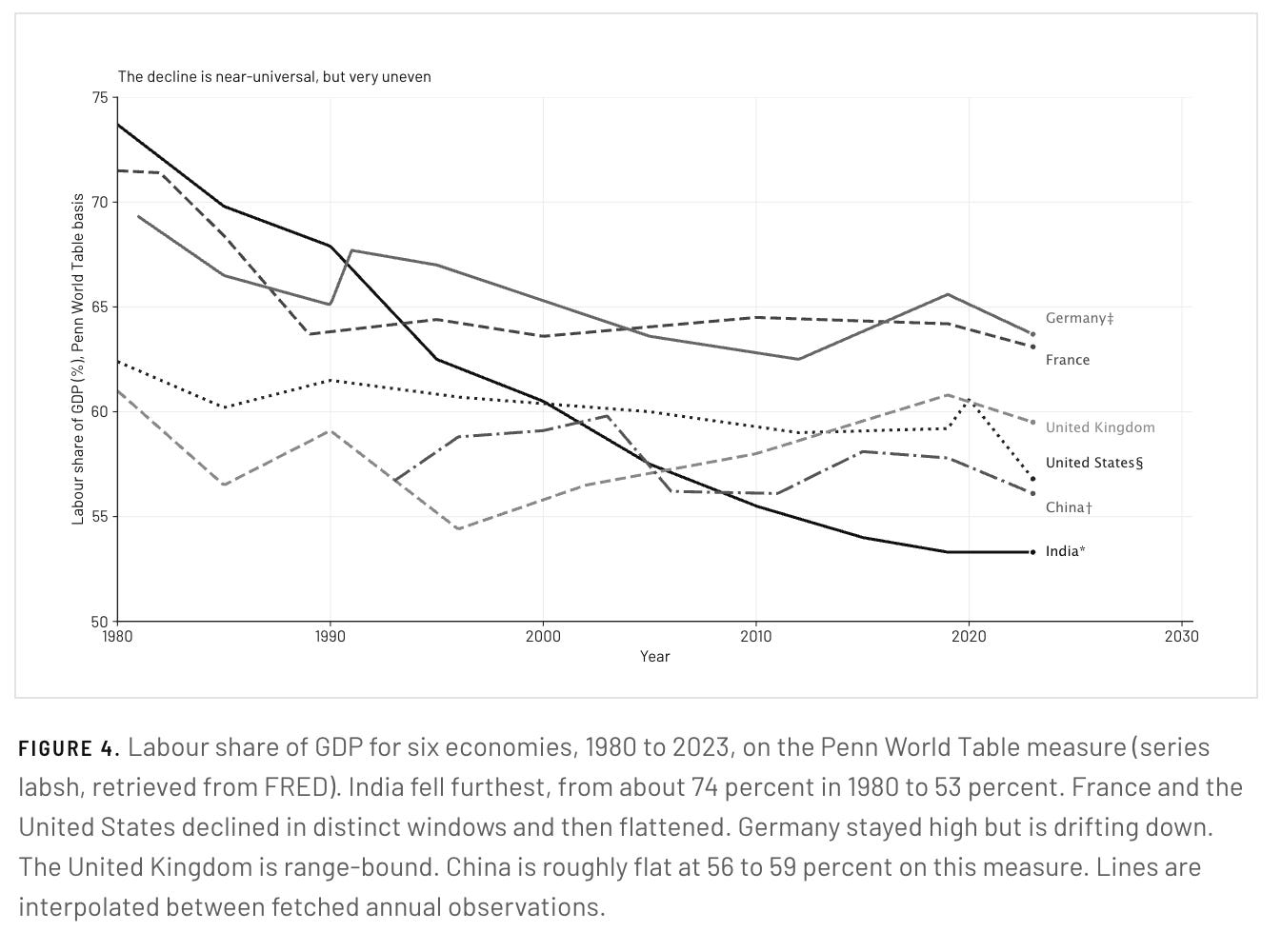

The same pattern is not confined to the United States. On a consistent cross-country measure, the Penn World Table’s share of labour compensation in GDP, the major economies all show the labour share flat or falling over the past four decades. None shows it rising. What differs is the size and timing of the fall.

The labour share is never trending up, across very different political economies, capitalist and state-capitalist, rich and developing.

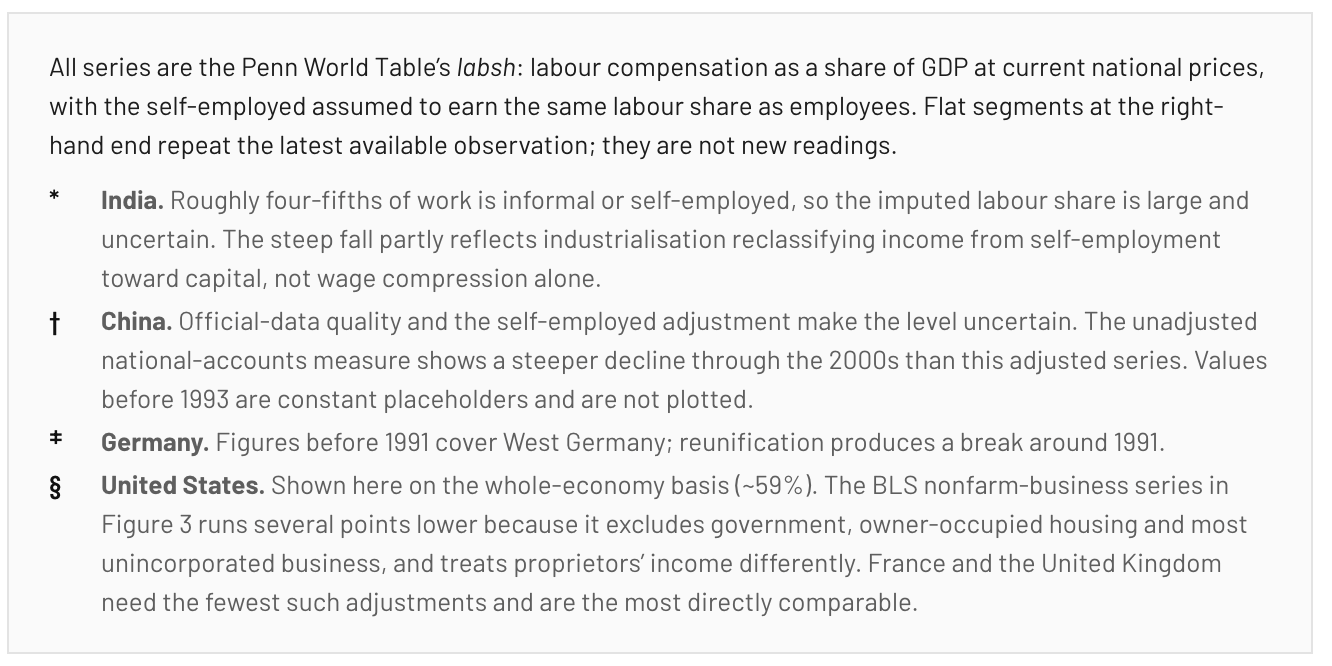

The caveat: this chart uses a single consistent source so the lines can be compared, but cross-country labour-share levels are still not strictly comparable, particularly for India and China, because the treatment of the self-employed, informal work, and indirect taxes varies by country. India’s steep fall reflects industrialisation pulling income from a vast self-employed agricultural base toward capital. China’s apparent stability on this measure is almost entirely methodological: the Penn World Table adjusts for the self-employed, while the unadjusted national-accounts measure shows China’s labour share dropping much more in the 2000s. And as the notes above set out, the whole-economy basis also puts the United States a few points higher here than its business-sector figure in Figure 3. In other words, the trajectories hold; the exact levels do not.

Owner consumption cannot fill the gap

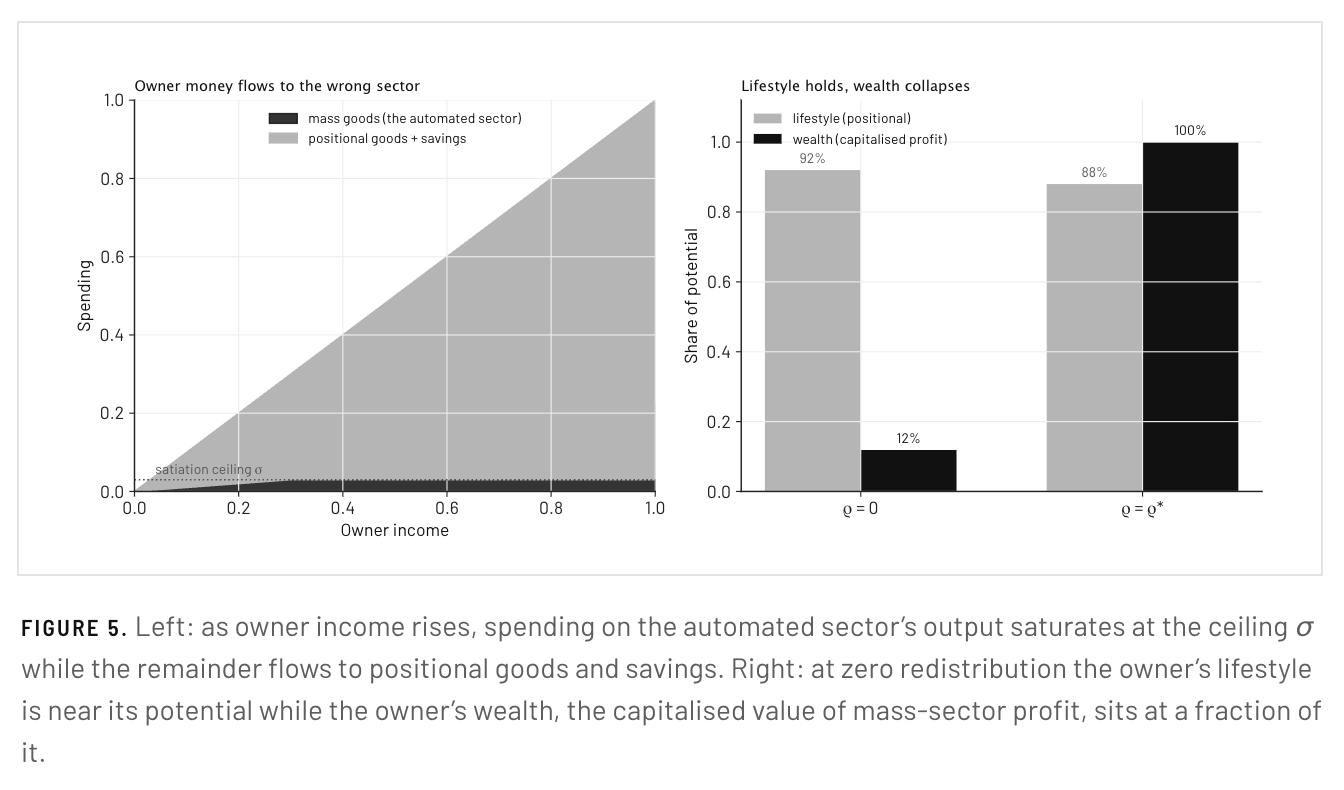

The first objection to the idea that demand collapses without redistribution is that owners consume too, so the demand floor is not negligible. The objection underweights two facts. As capital flows onto larger and larger balance sheets, driven by production-side network effects (robots build robots, agents build agents), owners are few. And physical consumption saturates: a billionaire cannot drink more cola than a delivery rider, so owner demand for mass goods hits the low ceiling σ regardless of wealth. The income above that ceiling does not buy mass output either. It flows to positional goods, the scarce things whose value is partly that they cannot be mass-produced, and to financial assets. Neither channel empties the warehouses of the automated sector.

This separates two things that are usually conflated. An owner’s lifestyle is satisfied at any redistribution rate by the self-contained world of positional goods. An owner’s wealth is the capitalised value of mass-sector profit. The two come apart.

Refusing redistribution does not cost the owner their comfort. It costs them their fortune.

An owner can live magnificently at zero redistribution while the value of everything they own quietly evaporates, because nobody else can buy their products.

The “human” economy is a real bridge, but it cannot scale

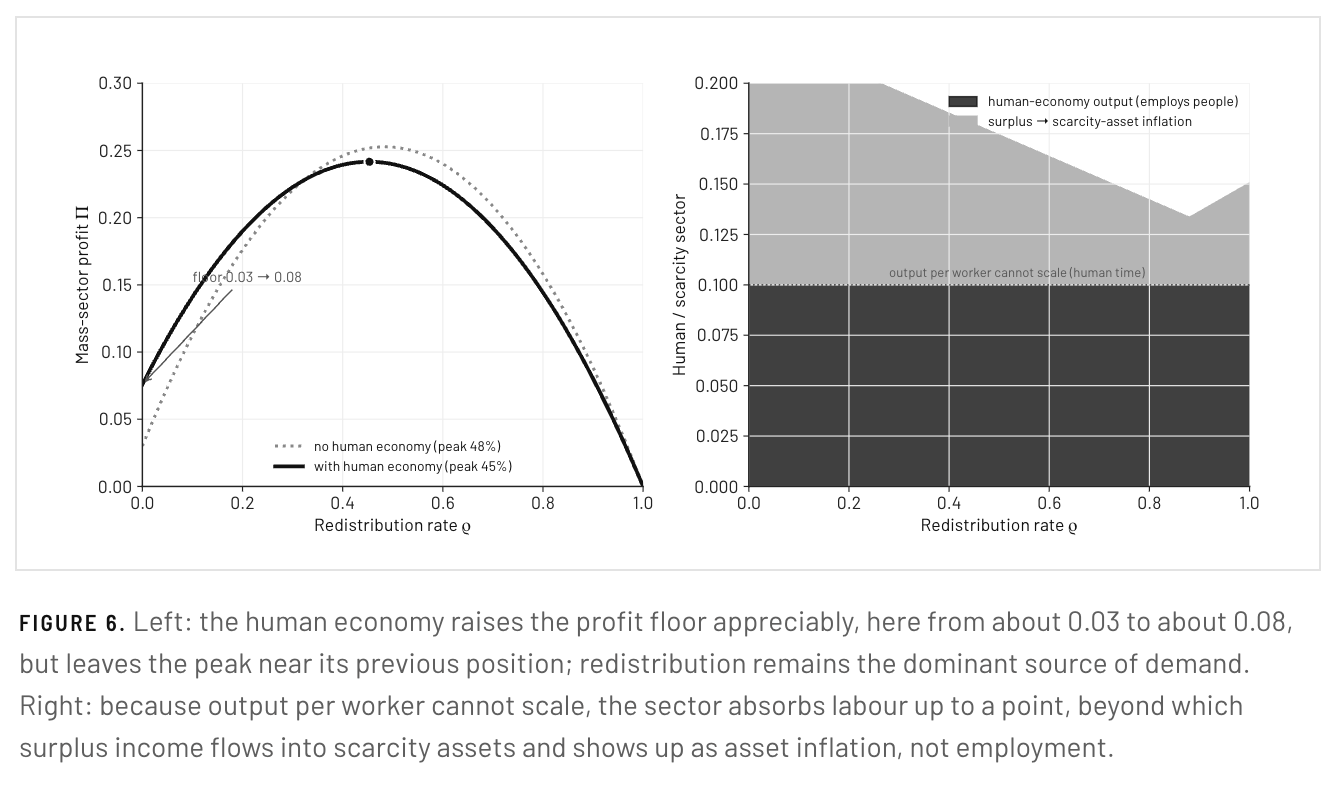

The second objection is more nuanced, and it points at something real. The capital that does not buy mass goods does not in turn all vanish into asset prices. A large part of it buys human experience: a live band instead of a stream, a haircut with conversation, a meal cooked and served in the room, care, teaching, coaching, craft, hospitality. These are valued precisely because a person does them, present and in real time. This is not a servant economy for the rich. It is the part of the economy that stays human, and ordinary people are its customers as much as anyone, because you buy haircuts and concert tickets too.

The defining property of human services is that they are labour-intensive and, by definition, less mass-producible. A barber cuts one head at a time; a band plays live at one event. Output per worker does not scale the way automated production does. That has two consequences for the model. Because the sector is labour-intensive, money spent on it becomes wages, and those wages are spent again, mostly on mass goods, so it recycles demand back to the automated sector. And because ordinary people are its customers, a redistributed pound spent on a haircut becomes the barber’s wage and is partly spent again, so the human economy multiplies redistribution instead of competing with it.

This is why the human economy lifts the floor without moving the peak, and why it cannot replace redistribution. It recirculates income without growing the pie at the rate the automated sector does. Someone must inject the extra income the human economy then passes around, and with mass-production wages gone, the only injectors are the owners, bounded by their number and their satiation even for experiences, and redistribution. And because human work cannot scale its output the way machines can, the sector employs people but does not manufacture the abundance that has to be cleared. Machines make the abundance; humans make the experiences; the demand problem is about clearing the abundance, and only income in ordinary hands does that. The escape that would let owners sustain demand purely by paying for human services closes itself: a human economy large enough to do that needs an income source to prime it, and that source is the very redistribution it was meant to avoid.

As the labour share falls, revenue has to come from capital

The labour share is a measure of primary income, the income earned in production and split between labour and capital. Welfare, pensions, unemployment benefits and a universal basic income are not in that split. They are secondary income, redistribution: the state takes primary income through tax and pays it out again to someone else. Transfers never appear in the labour share, because the labour share is the snapshot taken before the state moves anything around. In the model, this secondary layer is exactly what ρ represents, and a person on welfare already appears in the demand model as a recipient who spends; they earn no factor income.

Most of the state’s revenue, and almost all of what funds transfers, is currently raised from labour income through income tax and payroll tax. If the labour share falls, the base for those taxes falls with it. You cannot indefinitely finance a rising bill for transfers out of a wage base that is shrinking as a share of output. The money the state spends has to be raised against the income that actually exists, and a growing fraction of income accrues to capital.

A falling labour share both creates the demand gap and defunds the usual way of closing it. The revenue base has to shift to capital regardless of the demand argument

So two independent lines arrive at the same place. The demand argument says redistribution from capital is what keeps profit alive. The fiscal argument says that even to fund the existing functions of the state, revenue must increasingly be drawn from capital, because labour income is no longer where the money is. The question stops being whether to draw revenue from capital and becomes how to do it with the least damage.

Tax-funded transfers versus publicly held equity

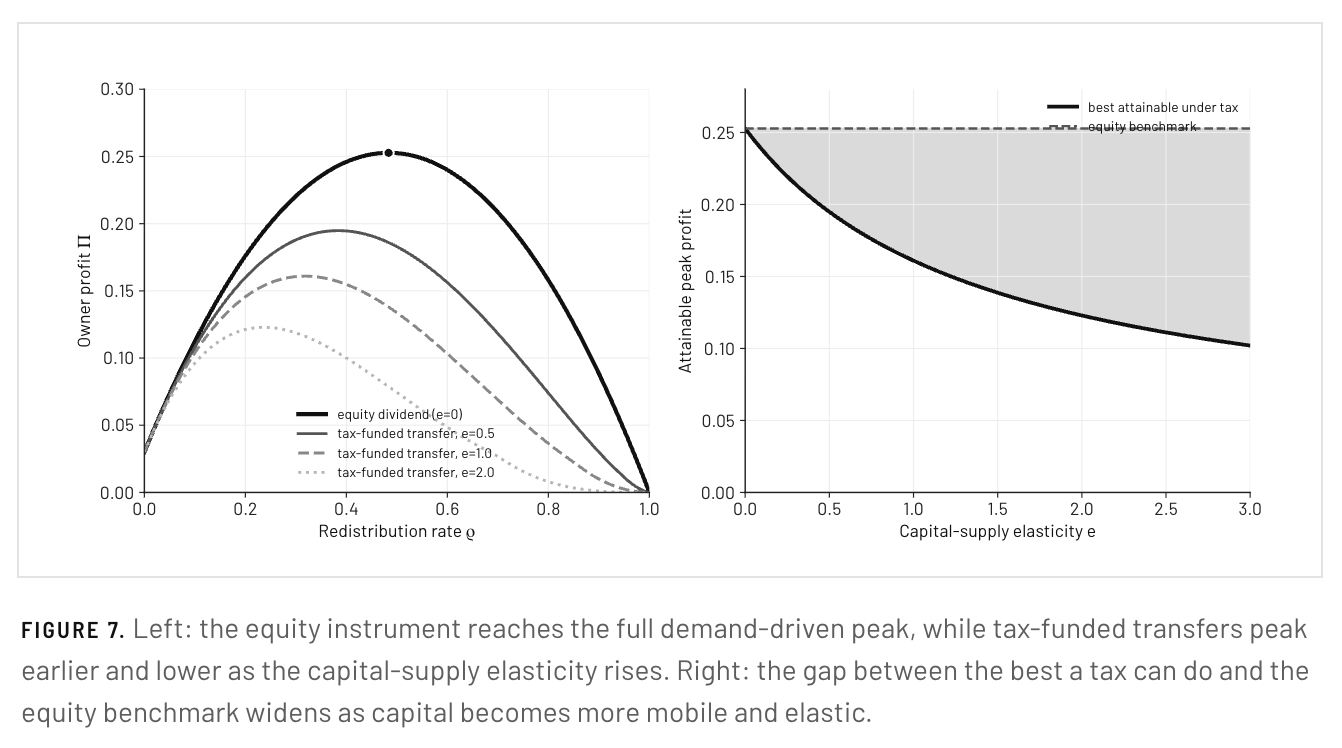

If revenue must come from capital, the form matters. The demand mechanism is blind to the source of a redistributed pound: a transfer cheque and a dividend cheque buy the same goods. The two instruments differ in the supply-side cost of reaching a given redistribution rate.

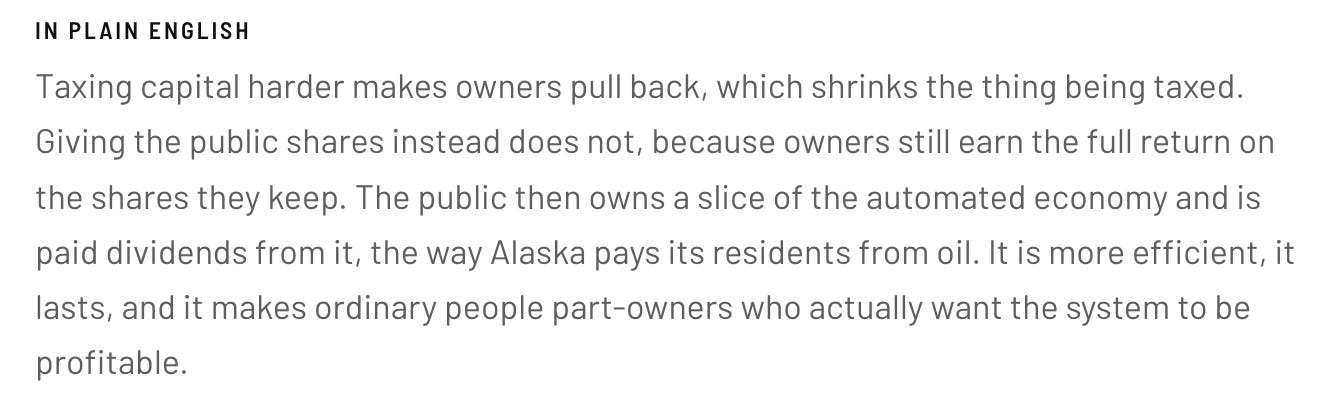

A tax on capital income is distortionary in the Laffer sense. Raise the rate and the base shrinks, because owners deploy less capital, automate less aggressively, and book profit elsewhere. Write capacity as Y(ρ) = (1 − ρ)e, where e is the capital-supply elasticity, the demand-side cousin of Laffer’s own parameter. Equity dilution does not do this. Handing the public a share ρ of the automated sector, held in a sovereign fund and paid out as a universal dividend, is a one-time transfer of stock. The return per share is unchanged, so owners keep deploying capital. It behaves like a tax on rents rather than on marginal returns: the same demand benefit, with little of the deadweight.

The advantage grows with how elastic capital is, and in an automated economy capital is software, models, and intellectual property, the most relocatable assets ever created. The regime where this curve matters most is therefore the regime where the tax instrument bleeds most and equity dominates by the widest margin. Three further properties point the same way. Equity is durable: transferred once, the dividend then tracks profit automatically as the labour share falls, where a transfer must be re-legislated every budget. It attacks the cause, because spreading ownership puts income into high-propensity hands at the source instead of skimming a flow to compensate after the fact. And it makes the central reframe literal. A taxed owner must be persuaded into enlightened self-interest; a citizen who owns a share is a residual claimant who already wants mass-sector profit to be high, because they own a piece of it.

The Alaska case

The design is not hypothetical. The Alaska Permanent Fund has held the state’s resource wealth as a sovereign investment fund and paid every resident an annual dividend for four decades. It is durable across the political spectrum, and residents spend the dividend as income instead of banking it as capital. That last point is the one place a transfer could have won, because dividends hoarded as wealth would weaken the demand effect the curve depends on. Alaska shows that a dividend framed and paid as income is spent as income. A sovereign fund holding equity in the automated sector and paying a universal dividend keeps the efficiency and durability of equity while matching a transfer on demand.

The band the economy has to sit in

Put the two curves together and they bound a window. Below a floor, redistribution is too low: demand fails, output goes unsold, and profit collapses. This is the demand-side result of this whole note. Above a ceiling, taxation is too high: the base shrinks and output falls. This is Laffer. A viable automated economy has to operate between the two. The instrument decides how wide the window is. Because taking equity is in effect a wealth tax on the capital stock rather than a levy on its income, it does not trigger the marginal base-erosion that sets the Laffer ceiling, so it raises the ceiling and widens the band. Income tax narrows it. The same redistribution can sit comfortably inside the window when done through equity and breach the ceiling when attempted through tax.

The economy must sit between a demand floor and a Laffer ceiling, and equity ownership is what widens the gap between them.

US 20th century capitalism as demand-side socialism

Most economies never settled the contest between capital and labour by choosing a side. They became mixed: a welfare state alongside free markets. But there is a contrarian way to read even the most market-oriented of them. Mass-production capitalism was already a kind of socialism, run from the demand side.

Mass production only pays if there is mass consumption. The twentieth-century economy worked because the aggregate purchasing power of ordinary people exceeded that of the elite, and it was that broad purchasing power, not the wealth of owners, that the system was built to serve. The masses were the market. Their spending was the point.

The cultural signature is unmistakable. The Soviet Union preserved an elite high culture handed down from above, the ballet and the symphony. The market democracies threw up a mass culture bought from below, the movies, jazz, rock and roll, made for and paid for by the many. Warhol caught the economics of it exactly: a Coke is a Coke, the President drinks the same one as Elizabeth Taylor and the same one as the bum on the street, and no amount of money buys a better one. Broad purchasing power flattened consumption into something shared. That is demand-side socialism: not the state owning production, but the many holding the purchasing power that production depends on.

Set this against the older, supply-side answer. Twentieth-century labour secured its position through the supply of work: ownership and control of the means of production, and the collective bargaining of unions, an equilibrium between capital and labour enforced by labour’s ability to withhold itself. That equilibrium was adversarial by construction, a balance of opposed powers. Demand-side socialism is different in kind, because the interests align. Capital needs the masses to be able to buy, so broad prosperity serves the owners themselves; no one has to wring it from them.

Full automation destroys the supply-side equilibrium. When labour is no longer needed in production it has nothing to withhold, and unions and the ownership struggle lose their leverage, because there is no productive role left to bargain over. What survives is the demand side. People are still needed as customers even when they are not needed as workers. The redistribution curve is the mechanism that keeps the demand-side alignment intact once the supply-side one is gone. It carries the mutual interest, capital wanting the masses to be able to buy, into an era when the masses no longer earn that ability through work. Equity ownership restores the purchasing power at its source, which makes the alignment literal: the public are customers and owners at once, wanting the same thing.

What there is to argue about

Laffer propogated as a concept because it reduced to one measurable, disputable number. This model does the same, with one headline parameter and three underneath it.

The headline is the labour share and, more precisely, its trajectory. It is measured and published quarterly, so the fight is not over its existence but over where it is heading: whether automation relocates labour and the share stabilises, or whether it falls further. That is the same shape of argument as Laffer’s elasticity, conducted over a number anyone can look up.

Three second-order parameters are the fallback positions:

The consumption-propensity gap between owners and everyone else, which sets how pronounced the hump is. No gap, no curve.

The owner satiation floor and the labour-intensity of the human economy, which together decide how much of the gap private spending can fill. The structural answer is that human work recirculates income but cannot mass-produce, so it softens the gap without closing it.

The capital-supply elasticity, which sets how much worse a tax is than equity. It is Laffer’s own parameter, reappearing from the other side, so the two curves end up arguing over the same quantity.

Note what is not the number to argue about: the optimal redistribution rate itself, or the size of the public equity stake. That is the model’s output, not its input, in the same way the top of the Laffer curve is a consequence of the elasticity, not a primitive. Leading with a target share states a conclusion with the reasoning amputated, and it reintroduces the moral register the whole argument is built to avoid. The labour share is a diagnosis, not a demand. The redistribution rate follows as an implication.

The whole argument, in order

Profit, like revenue, is bounded and humped, but on the redistribution axis instead of the tax axis, with the right end pinned at zero and the left end low. The labour share is the dial that selects the regime, and it has fallen from about two thirds of output to about half, almost all of it since 2000. It can now fall further than it ever has, because AI automates the cognition that earlier machines still required, removing the complementary human role that kept the share stable for a century. Owner consumption cannot fill the resulting demand gap, because the rich are few and their money flows to positional goods and assets. The human economy recycles some of it and is where work goes as machines take over, but it moves income around, creates none, and cannot mass-produce, so it lifts the floor without moving the peak. Independently of all this, a falling labour share erodes the wage-tax base, so revenue must shift to capital regardless. And the least damaging way to draw revenue from capital is to spread its ownership: a sovereign fund holding equity in the automated sector, paying a universal dividend, on the Alaska model. Where the last century aligned capital and labour on the supply side, through unions and the ownership of machines, a settlement that automation dissolves, this keeps them aligned on the demand side, through the purchasing power that mass production has always quietly depended on.

The argument does not ask the owners to be good. It asks them to be smart, and it makes the public into owners who want the same thing they do.

Build before you redistribute

One caveat governs everything above. It sits at the end because it is about sequence, not substance. This describes where a mature automated economy ends up; it is not a programme for today. Redistribution presupposes something to redistribute, and the efficient instrument, taking equity in the automated sector, presupposes more: it requires sovereign firms to take equity in. A polity that taxed or socialised heavily before it had built competitive companies of its own would have nothing to take equity in, would be forced onto the inefficient tax route against firms it does not own, and would most likely strangle its own industry before it existed, driving capital and talent elsewhere.

The sequence is not optional. First build sovereign capacity in the automated sector; only once it is generating returns does redistributing from it make sense. Doing it in the other order is not redistribution but pre-emptive surrender, and for somewhere like Europe, tempted to regulate and tax an industry it has not yet created, it would be self-defeating. The whole argument assumes the value exists and is domestically owned. Getting there comes first.